The Nature of Venture

This essay appeared first in Messari, read the full piece on our site.

The nature of venture capital is changing. While the venture capital industry has origins dating back to the 19th century, the concept exploded in the 1960s after the successful backing of semiconductor startup, Fairchild Semiconductor. While capital – the ability to source millions of dollars – was initially the primary source of value, access to capital has become increasingly commoditized.

The maturation of the internet and the advent of crypto only further accelerated the commoditization of capital with the ability to easily distribute information and transfer value, respectively. As the crypto industry matures, the venture industry is finding its footing unbalanced as venture capitalists experience the rug being pulled out from underneath them. These are the warning signs of venture’s next evolution.

The Canary

Looking back, PoolTogether – the no-loss lottery protocol – acted as the proverbial canary in the coal mine for what was to come in future crypto funding rounds. PoolTogether Improvement Proposal 11 aimed to raise $7 million for the PoolTogether protocol in exchange for 5.38% of the total POOL supply. The strategic round would include a few venture funds receiving tokens at a 35% discount with a one-year lock up, followed by one-year weekly vesting (effectively two years until fully distributed). The community was upset. In May the market was still frothy (ETH trading at ~$3,000) but POOL was trading rather sideways and the PoolTogether community felt as if they were getting a raw deal, with most of the community members unable to participate.

Since the strategic round was relatively small and there were only four venture funds included in the round, the community and VCs were able to come to an amicable agreement, in large part because of PoolTogether founder Leighton Cusack who was able to liaison a better deal (PIPT-13) for the community. The new deal reduced the deal size to ~$6 million with a 30% discount, brought in Maven Capital, a European-based VC who committed to depositing working capital into PoolTogether’s protocol. In the end, the PoolTogether community spent 76% of the token allocation from the first deal (24% savings rate) while receiving 85% of original capital (a loss of only 15%). The PoolTogether community’s ability to push back and force VCs to the negotiation table demonstrates the shifting power dynamics of open, liquid cryptonetworks.

But, alas, the warning signs only grow.

The First Tremor

SushiSwap, a decentralized Exchange with nearly $3 billion more capital locked in its protocol than PoolTogether has elevated PoolTogether’s experience in funding, community backlash, and entertainment.

For context, Sushiswap is similarly conducting a strategic round from its treasury to a group of venture investors.

You can read the whole thread if you want, but you’ve been warned.

The deal terms:

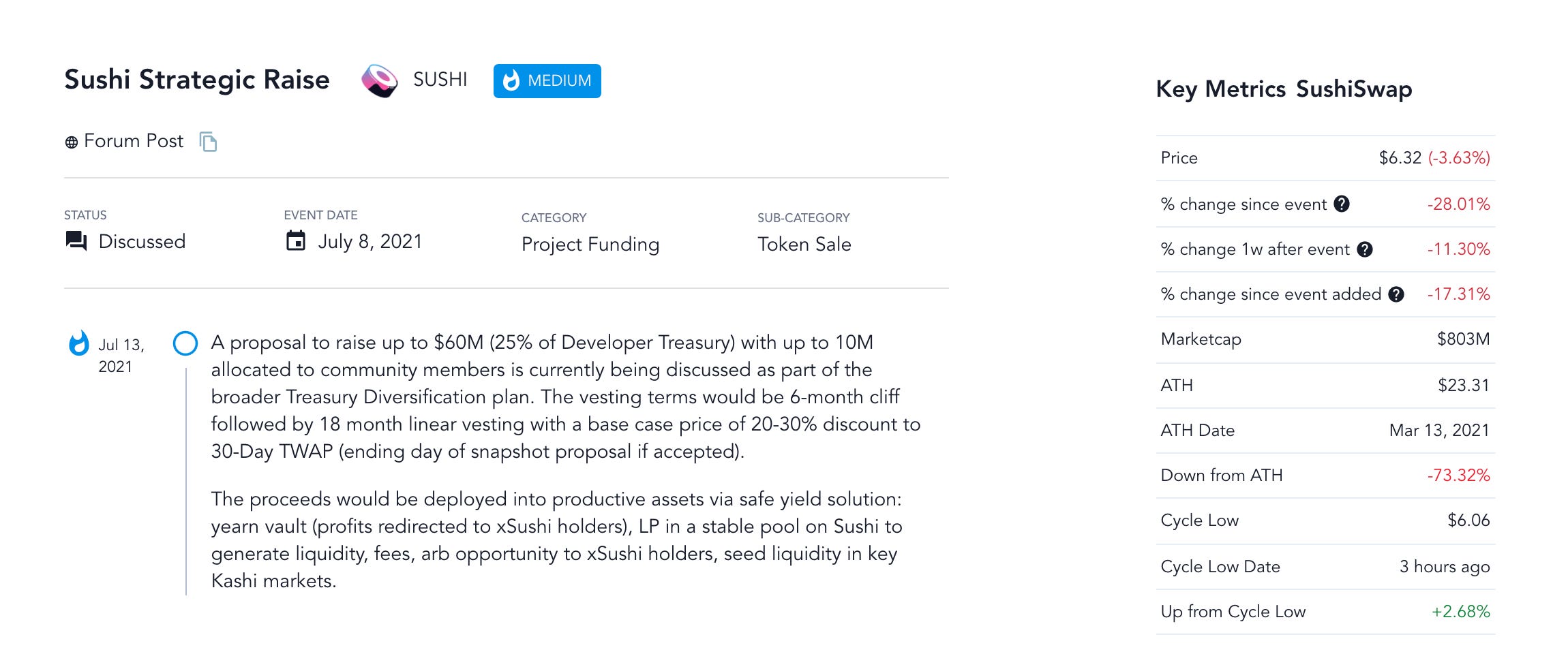

Deal size: $60m (25% of Developer Treasury) with up to 10m allocated to community members.

Vesting: 6-month cliff followed by 18-month linear vesting

Discount of 20-30%

SushiSwap’s round was to be co-led by Pantera and Lightspeed Venture Partners, the latter of which placed one of the best VC bets of all time. Even with a portion of the round allocated to the community, individuals were still upset. In the over 268 comments left, many are from community members sharing how the discount is unfair, the round too large, the vesting schedule too short, and the value proposition vague.

Many of the venture funds including both co-leads responded to the criticism explaining the reason for the discounts and the value that venture funds can bring to fishy DEX. (Lightspeed initial response, Pantera).

Generally speaking the top reasons for why venture funds can provide value include:

Get working or growth capital

Use the VC's connections and relationships

Signaling (brands help)

Other advice, support, guidance

Encourage other portfolio companies to partner with the protocol

Secure other long term partners, including partners in the traditional financial realm

Generally speaking, in both the PoolTogether and Sushi strategic rounds, venture funds advocate that discounts are fair because of the capital lockup and the value these funds can provide to the protocols. However, even as funds in the Sushi forum explained how the capital lock-up deserved the discount and aligned long-term incentives, members of the Sushi remainedunconvincedthatall 20 funds would equally provide the same value or that the short lock-up would equate to long-term players.

The Sushi community’s intuition that not all funds would be long-term players was somewhat accurate. Defiance Capital immediately started selling (you know, in order to be better long-term investors and all) which was quickly noticed by Twitter. Notably, DeFiance responded, stating that they have a fiduciary responsibility to sell tokens and that their actions don’t need to be explained to the public.

Still, I wholeheartedly believe that venture funds can provide value when interests are long-term aligned. FutureFund spent a few million on the “sushi.com” domain for SushiSwap. SBF and Alameda have been long supporters of Sushi from the beginning. Other VCs are great at recruiting, sourcing deals, and connections are more important than people realize. But this value is often “soft” – interpersonal – rather than “hard” – actual technical development work – and as such is hard to communicate.

The Sushi Community is understandably upset, a bunch of VCs swoop in for a sweet 30% discount with a 15-month lockup. Most Sushi community members would probably take that deal!

Thankfully, the venture investors heard the outrage and responded accordingly. SBF posed good solutions including 2x lockup which justifies the discount and long-term incentives. Amy Wu from Lightspeed agreed to remove the discount and extend the lockup.

All seemed calm and headed towards a resolution, until Jeff Dorman entered the chat.

Jeff’s investment management firm, Arca, is long fish coin. It holds 7.5% of the SUSHI supply, all purchased on the open market. Arca countered the strategic round proposal with an offer to purchase up to $10 million SUSHI at a 30% premium to the current price on July 16th. The firm claims that SUSHI trades below its fair market value and as such shouldn’t be selling a large percentage of the treasury. Additionally, the counter offer proposed that SushiSwap wasn’t in need of $60 million and instead, that $10 million should be more than enough to use for operations or deploy as stablecoins into the protocol.

There hasn’t been an update on the new proposal or any insights into whether both proposals will be equally considered (given that large individual token holders will likely determine the outcome). Still this situation is unprecedented and has sent shockwaves throughout Crypto Twitter resulting in a story with as many twists and turns and financial absurdity as a Money Stuff newsletter (here's your next subject, Matt Levine!) How the SushiSwap strategic round unfolds is still up in the air and regardless of what happens to SushiSwap, the takeaway is that the game is changing.

The Future of Venture

It's a testament to the power of crypto networks that world-renowned VCs like Lightspeed now have to approach the community for a fundraising round. The community has negotiated on behalf of their protocol, and it appears as if the strategic round will now increase the lockup while reducing the 30% discount. That’s value add from the Sushi community.

Ultimately the right decision – on whether to take venture funding and respective deal terms – changes with each protocol. Some protocols can more effectively use capital which means that raising more stablecoins will be useful. Other teams might want to pair with venture funds they know will deliver value like Paradigm or favor funds that will only back one horse in the race.

Venture can provide mercenary capital or value, and reputation will be a competitive advantage for venture funds. Some funds will nuke their reputations over single deals (after all, there’s still money to be made) while long term players will thrive with the additional publicity that comes from blockchains. VCs will increasingly face pressure from communities when they get cushy deals that don't come with significant lockups or funds will have to prove the value they bring is worth the discount.

The warning signs of the venture capital industry’s natural evolution are becoming more frequent. The deals are less private. The funding rounds are more competitive. The people are more powerful.

Ultimately, venture funds aren't going away, however, the nature of venture is changing.